Key Takeaways

- 99% of intercontinental traffic runs undersea. TeleGeography's 2026 Submarine Cable Map counts 694 cable systems and 1,893 landing stations. Satellites, including Starlink, still carry well under 1% of traffic between continents.

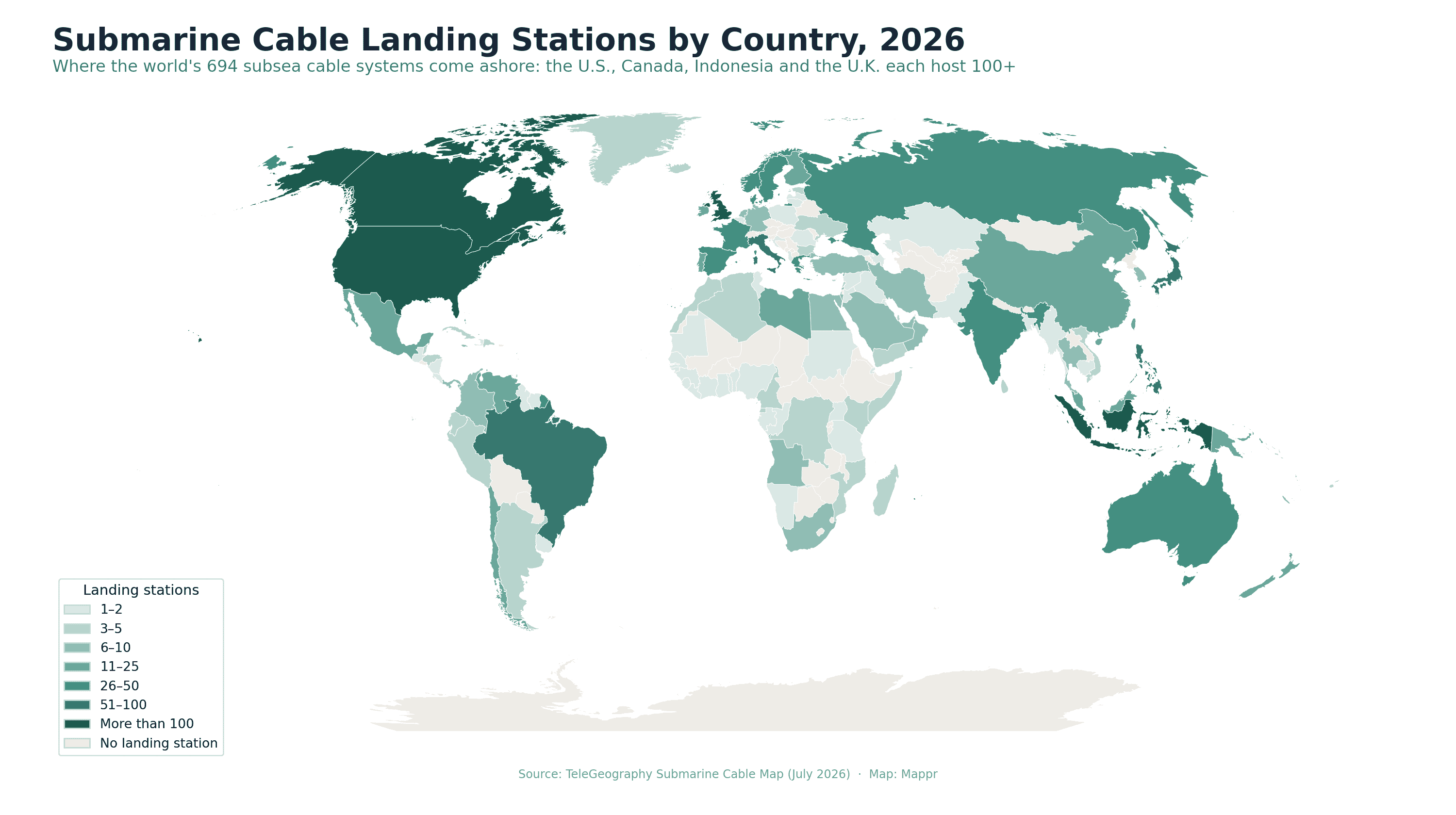

- The U.S. hosts the most landings. 167 landing stations and 115 distinct cable systems touch American shores, ahead of Canada (155 stations), Indonesia (143) and the United Kingdom (125).

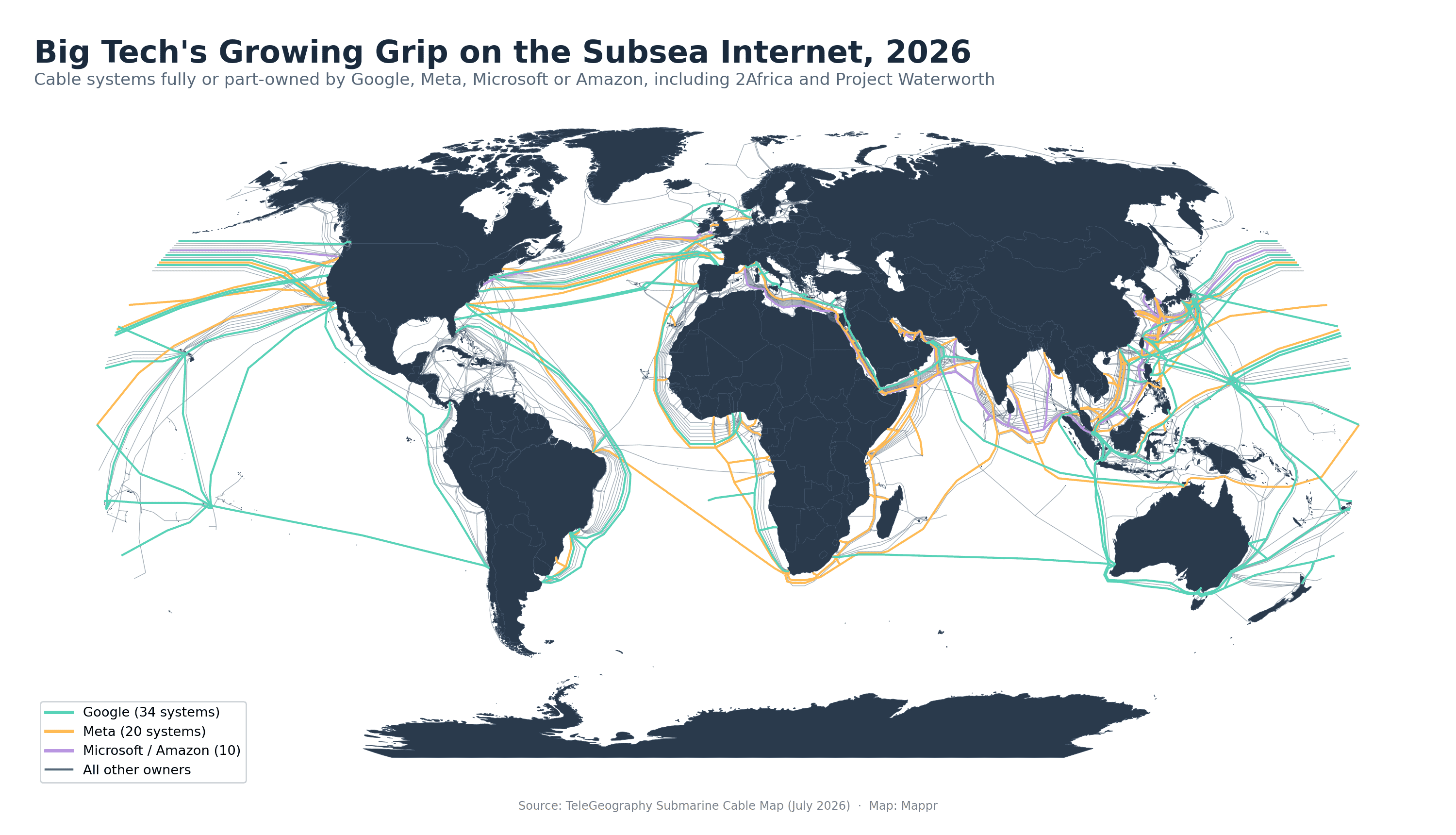

- Big Tech owns a growing share. Google has an ownership stake in 34 cable systems and Meta in 20. Hyperscalers now use roughly three-quarters of all international bandwidth, up from almost nothing in 2010.

- The Red Sea is the internet's most dangerous chokepoint. 14 active systems squeeze through the Bab el-Mandeb strait. After repeated cable cuts and Houthi attacks, work on 2Africa's Gulf extension was halted under force majeure in March 2026.

- A record buildout is underway. 33 new systems are slated for service in 2026 and 32 more in 2027, with roughly USD 13 billion flowing into new subsea projects between 2025 and 2027.

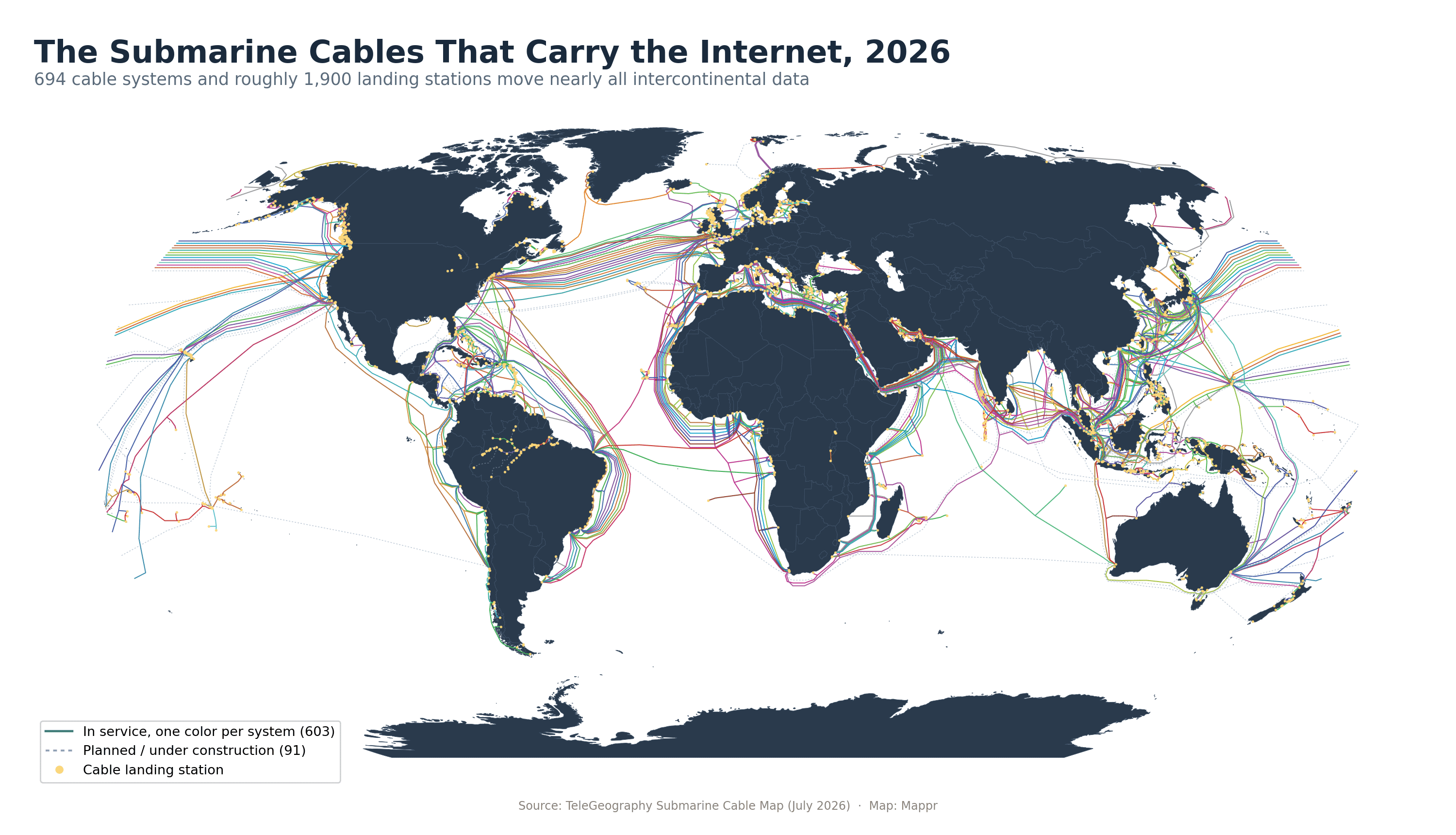

Every WhatsApp message to another continent, every international Zoom call, every dollar of cross-border cloud computing rides a fiber-optic tube no wider than a garden hose, lying on the seabed. According to TeleGeography’s 2026 Submarine Cable Map, the 30th annual edition of the industry’s reference chart, that hidden network now spans 694 cable systems connected through 1,893 landing stations, and it carries more than 99% of all intercontinental data traffic.

We pulled TeleGeography’s full open dataset (July 2026) and mapped the physical backbone of the internet three ways: every cable route on Earth, the countries where cables come ashore, and the corporate owners behind them. The result shows an internet that is far more concentrated, and far more fragile, than most people assume.

One Map of the Internet’s Physical Backbone

Of the 694 systems in the dataset, 603 are in service and 91 are planned or under construction. The pattern is unmistakable: dense bundles cross the North Atlantic and North Pacific, hug the coasts of Africa and South America, and converge on a handful of maritime chokepoints, the Suez corridor, the Strait of Malacca and the Luzon Strait among them.

The network is also strikingly redundant in some places and terrifyingly thin in others. More than a hundred systems connect the wealthy North Atlantic rim, while 25 countries and territories, from Sierra Leone and Gambia to Vanuatu and the Solomon Islands, still depend on a single cable for their connection to the global internet.

Landing Stations by Country

Counting where cables physically come ashore produces a few surprises. The United States leads with 167 landing stations, but Canada sits second with 155, ahead of Indonesia (143) and the United Kingdom (125). Long coastlines and domestic island-hopping networks inflate those numbers: most Canadian, Norwegian and Philippine stations serve short coastal festoon systems rather than intercontinental trunks.

The physical internet

Landing Stations by Country, 2026

Unique cable landing stations per country in TeleGeography’s July 2026 dataset. Excludes stations marked as not yet determined.

| Country | Landing stations | Notes |

|---|---|---|

| United States | 167 | 115 systems; both coasts plus Guam and Hawaii |

| Canada | 155 | Mostly domestic coastal and Arctic links |

| Indonesia | 143 | 72 systems stitch 17,000+ islands together |

| United Kingdom | 125 | Europe's transatlantic front door; 65 systems |

| Brazil | 74 | South America's hub; 25 systems |

| Philippines | 71 | Archipelago networks plus trans-Pacific landings |

| Japan | 68 | 50 systems; the Pacific's western anchor |

| Italy | 55 | Mediterranean crossroads for Asia-Europe routes |

| Spain | 48 | Atlantic and Mediterranean gateway |

| Norway | 42 | Coastal festoons plus Arctic ambitions |

| Greece | 36 | Eastern Mediterranean branching point |

| Denmark | 34 | North Sea and Baltic junction |

| Russia | 28 | Mostly domestic Arctic and Far East links |

| Sweden | 28 | Baltic Sea connections |

| France | 27 | 34 systems; Marseille is Europe's southern gateway |

A note on method: TeleGeography counts a handful of inland points, such as Kampala in Uganda, as landing stations where cables extend overland, and the Caspian Sea hosts genuine subsea landings in Kazakhstan and Azerbaijan. We count each unique station once, however many cables terminate there.

The Hubs That Matter Most

Raw station counts tell only half the story. A few countries punch far above their coastline in strategic terms.

🇸🇬 Singapore

With 43 distinct systems landing on an island of just 734 square kilometers, Singapore is the densest cable hub on Earth. Nearly everything moving between the Indian Ocean and the Pacific transits either Singapore or the Strait of Malacca beside it, one reason new systems like Google’s Apricot and Echo are deliberately routed around it, through Indonesia and the Philippines, to add diversity.

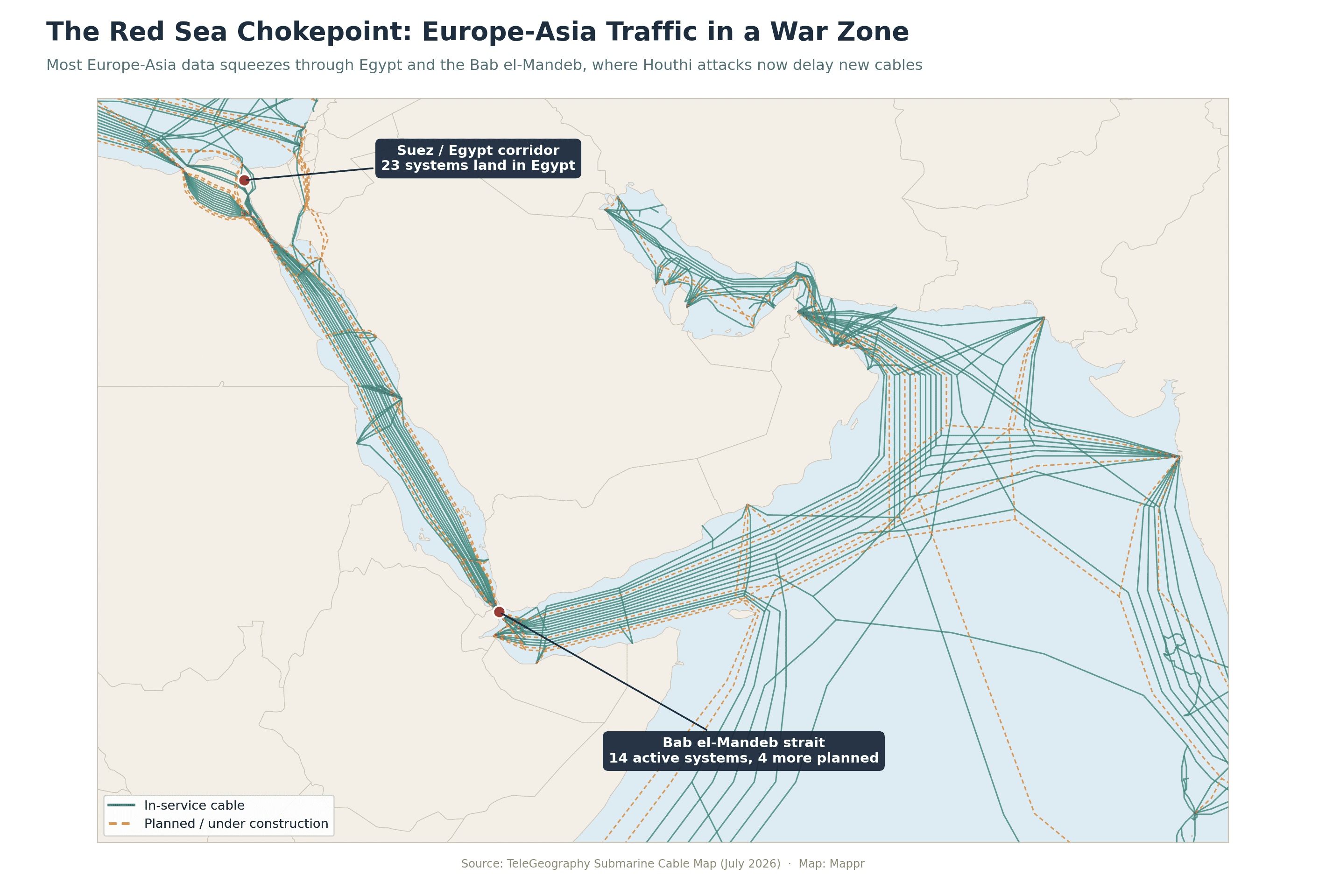

🇪🇬 Egypt

23 systems land in Egypt, where Europe-Asia cables cross roughly 200 kilometers of land between the Mediterranean and the Red Sea rather than sailing around Africa. Telecom Egypt charges famous premiums for the crossing, and TeleGeography made the state carrier the sponsor of its 2026 map, a nod to how central the corridor has become.

🇮🇳 India

India hosts 26 landing stations, concentrated around Mumbai and Chennai, and is the fastest-growing major destination: 2Africa’s Pearls branch, Meta’s Project Waterworth, Google’s Blue-Raman and the India Europe Xpress all target Indian landings. A billion users and a booming AI data-center market are pulling the network eastward.

🇺🇸 United States

Beyond hosting the most stations, the United States is where the money and the rules live. All four hyperscale cable investors are American, and in June 2026 the FCC unanimously approved the first major overhaul of subsea licensing in two decades, tightening security review while fast-tracking AI-era builds.

Who Owns the Cables? Big Tech’s Deep-Sea Land Grab

For a century, undersea cables were built by consortia of national telecom carriers. That era is over. Google now holds an ownership stake in 34 cable systems and Meta in 20, with Microsoft and Amazon on ten more between them. By TeleGeography’s reckoning, hyperscalers’ share of international bandwidth use has gone from almost nothing in 2010 to roughly 75% today, they control about 90% of trans-Atlantic capacity, and they are involved in over two-thirds of all planned deployments.

Three projects define the moment. Meta’s 2Africa, completed in its core form on 17 November 2025, is the longest cable system ever brought into service: 45,000 kilometers looping the entire African continent, with 46 landing stations in 33 countries and a design capacity of 180 terabits per second. Meta’s Project Waterworth will beat it: 50,000+ kilometers linking the United States, Brazil, South Africa and India across five continents, deliberately routed to avoid both the Red Sea and the South China Sea. Meta has published no completion date; reporting points to roughly the end of the decade. And Google’s Dhivaru, unveiled the same week 2Africa was finished, will tie the Maldives, Christmas Island and Oman together with new connectivity hubs in Addu City and on Christmas Island.

The concentration cuts both ways. Hyperscaler money is wiring up places carriers ignored, Saint Helena owes its fiber to Google’s Equiano, but it also means four American companies increasingly own the pipes their competitors and half the world’s traffic must ride. Critics note the map itself echoes the 19th-century telegraph network: the routes still run through the same colonial-era chokepoints, and much of Africa’s traffic still detours through Europe. For a sense of where all that data ends up, see our companion map of the countries with the most data centers.

The Red Sea: Where the Internet Goes to War

Fourteen active cable systems thread the Bab el-Mandeb strait between Yemen and Djibouti, with four more planned. It is the only practical wet path between Europe and Asia, and it runs straight through a war zone.

The risk stopped being theoretical on 24 February 2024, when the dragging anchor of the sinking cargo ship Rubymar, hit by Houthi missiles days earlier, severed the Seacom, EIG and AAE-1 systems in one pass, degrading roughly a quarter of Red Sea-region traffic. Repairs took months amid Yemeni permit politics. On 6 September 2025 it happened again: SMW4 and IMEWE were cut near Jeddah, slowing internet access across India, Pakistan and the Gulf and pushing up Microsoft Azure latency for hours.

By 2026 the insurance math had broken. Alcatel Submarine Networks declared force majeure on 2Africa’s Pearls extension into the Gulf in March 2026, leaving laid cable unconnected on the seabed and the lay vessel Ile de Batz idle off Dammam. The Raman half of Google’s Blue-Raman system, which would run Mumbai to the Gulf via the Red Sea, is delayed by the same security and insurance pressures, SeaMeWe-6 has slipped from 2027 to indefinite, and the USD 700 million WorldLink Transit project was cancelled outright. Waterworth’s route, which skips the Red Sea entirely, no longer looks conservative. It looks prescient.

What’s Being Built

None of this has slowed the buildout; it has redirected it. The dataset lists 33 systems scheduled for service in 2026, 32 in 2027 and 21 in 2028, and industry analysts expect roughly USD 13 billion in new subsea investment between 2025 and 2027, nearly double the previous three years. AI is the accelerant: training clusters on different continents need to move oceans of data between them.

The 2026 class includes Google’s Nuvem (Portugal-Bermuda-U.S.), Bulikula and Tabua in the Pacific, Meta’s Anjana across the Atlantic, the Medusa system spanning the Mediterranean, and Taiwan-Matsu No. 4, a resilience cable for the Matsu Islands, which have been cut off more than 20 times in five years, most recently in April 2026. Each incident near China‘s coast sharpens the same lesson the Red Sea taught: the internet’s weakest points are geographic, not digital.

For most readers the takeaway is simple: the cloud is not in the sky. It is 4,000 meters down, hand-buried by plows near shore, spliced by a global fleet of about sixty repair ships, and increasingly owned by four companies. The next time a country drops off the internet overnight, the explanation will almost certainly be on this map.

Data and references:

Data Sources:

News Sources:

- Meta Engineering: Completing the core 2Africa system (Nov 17, 2025)

- TechCrunch: Meta confirms Project Waterworth, a 50,000 km global subsea project

- Google Cloud: Introducing Dhivaru, a new trans-Indian Ocean subsea cable

- Capacity: Meta consortium pauses 2Africa Pearls cable work (force majeure)

- Kentik: What caused the Red Sea submarine cable cuts?

- Network World: Red Sea cable cuts trigger Azure latency across Asia and the Middle East (Sept 2025)

- IEEE ComSoc / TeleGeography: Hyperscalers' dominance of subsea cable capacity (June 2026)

- FCC: Submarine cable licensing modernization order (June 2026)