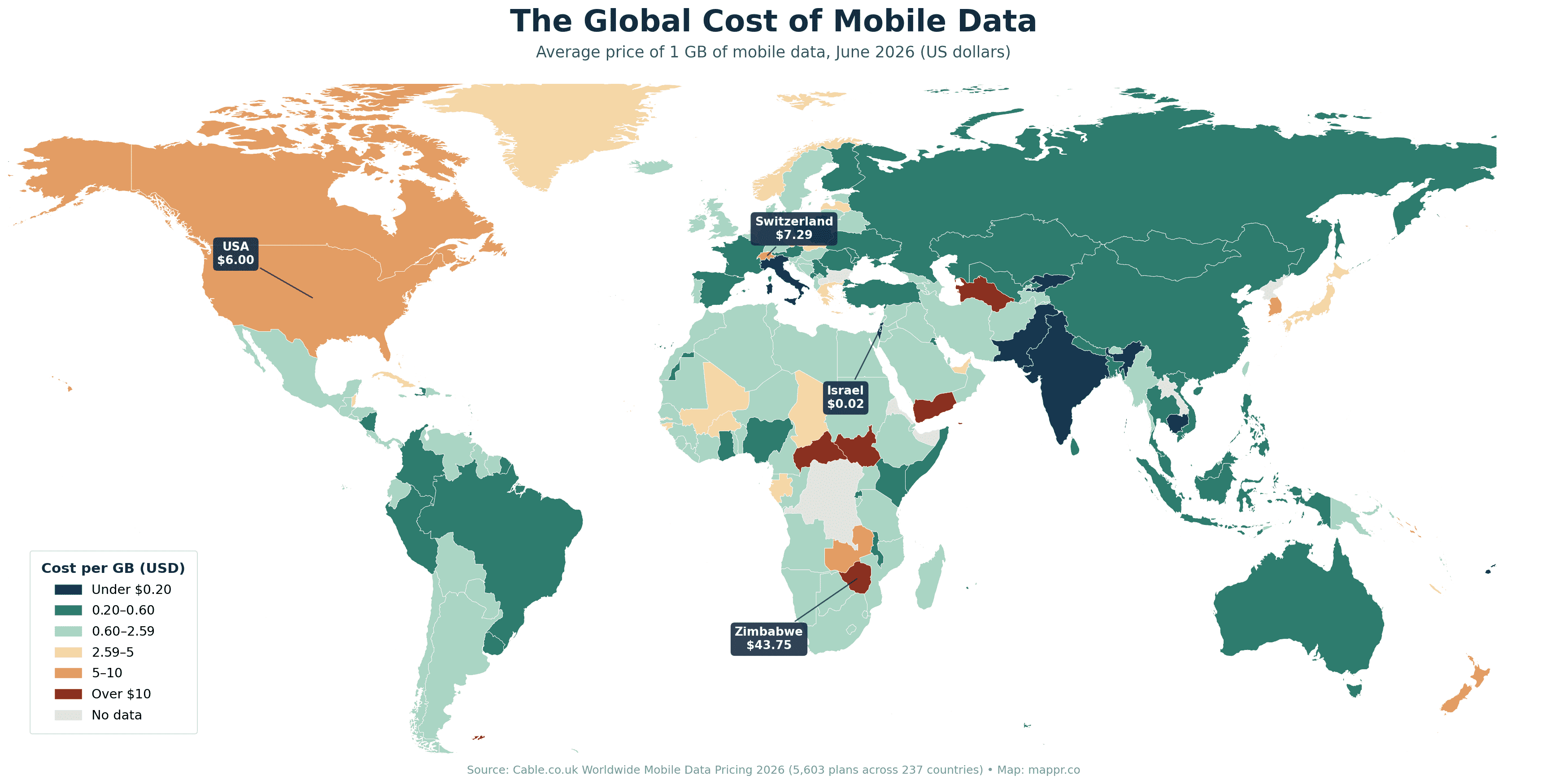

A gigabyte of mobile data costs $0.02 in Israel and $43.75 in Zimbabwe. That is a 2,000× spread from cheapest to most expensive, in the same year, for essentially the same product. The average price globally, across 237 countries and territories and 5,603 mobile data plans surveyed by Cable.co.uk in June 2026, is $2.59 per GB, down from $8.18 in 2019.

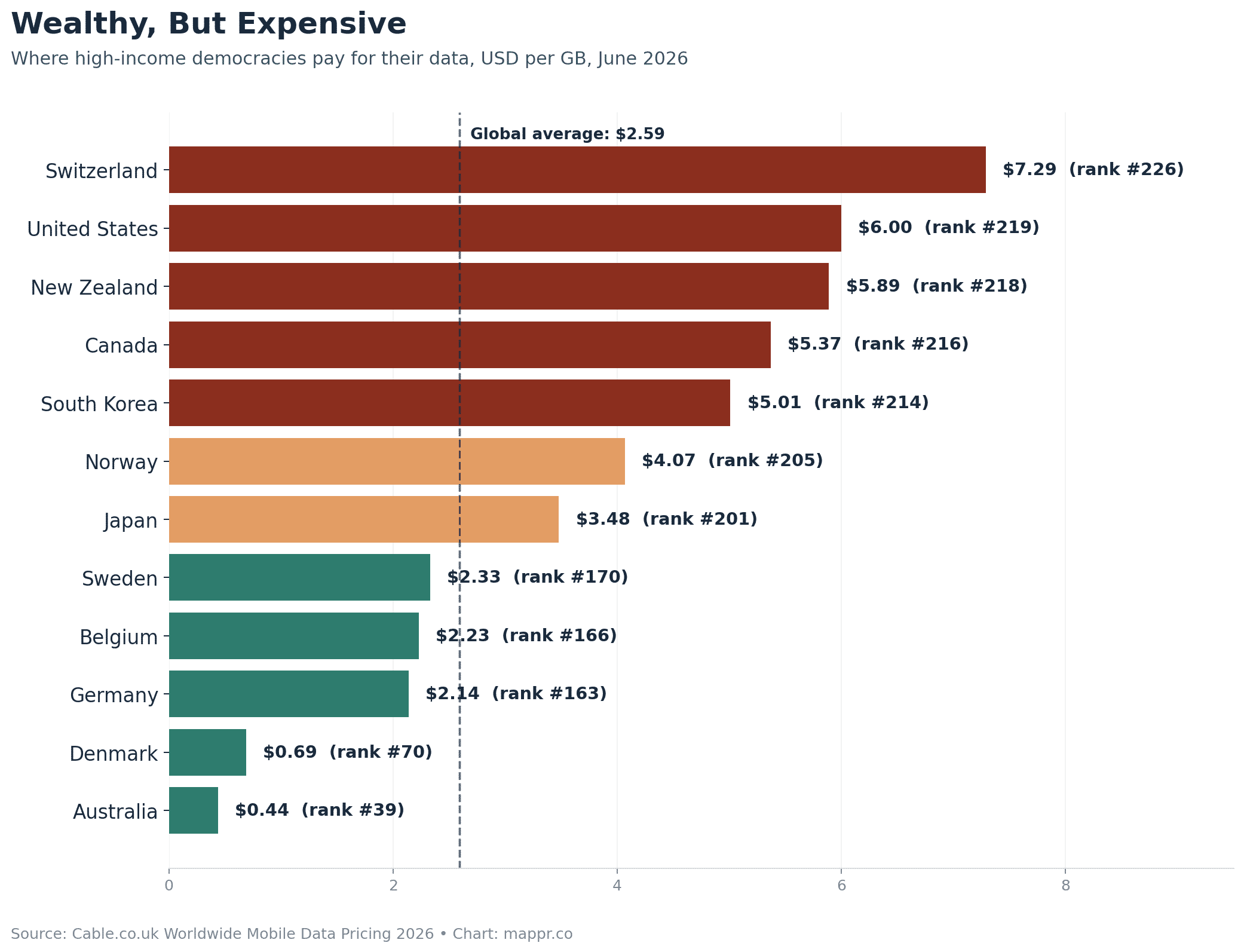

The story the numbers tell is not the one most Americans expect. The United States ranks #219 out of 237 at $6.00 per GB, more expensive than every other wealthy democracy except Switzerland ($7.29) and only marginally cheaper than Canada ($5.37) and New Zealand ($5.89). Meanwhile India, Pakistan, Cambodia and Kyrgyzstan all sit in the top ten cheapest. Below is the full map, the ranking, and a closer look at why the wealthy Western world pays such a premium.

Key Takeaways

- Israel is 2,000× cheaper than Zimbabwe. 1 GB of mobile data averages $0.02 in Israel and $43.75 in Zimbabwe. The global average across 237 countries is $2.59 per GB.

- The US is one of the most expensive markets. The United States ranks #219 out of 237 at $6.00 per GB, ahead of Canada ($5.37, #216) and just below Switzerland ($7.29, #226). All three are wealthy but pay far above the global average.

- Italy and Fiji share second place. Italy ($0.09) and Fiji ($0.09) tie for second-cheapest globally. Italy stands out as the only wealthy Western economy in the top ten cheapest.

- Africa still runs the priciest data. Nine of the ten most expensive countries have GDP per capita well below the global median. Zimbabwe, Saint Helena, South Sudan, the Central African Republic and Yemen all sit above $10 per GB.

- The global average keeps falling. Global average cost per GB has fallen from $8.18 in 2019 to $2.59 in 2026, a 68% drop in seven years. The gap between cheapest and most expensive has widened, not closed.

The Global Price Map

The choropleth below shades countries by average cost per GB, from teal (cheapest, under $0.20) to dark red (most expensive, over $10). The pattern is legible from a distance: Asia and southern Europe are cheap, sub-Saharan Africa and small remote islands are expensive, and North America is the standout wealthy-but-expensive block.

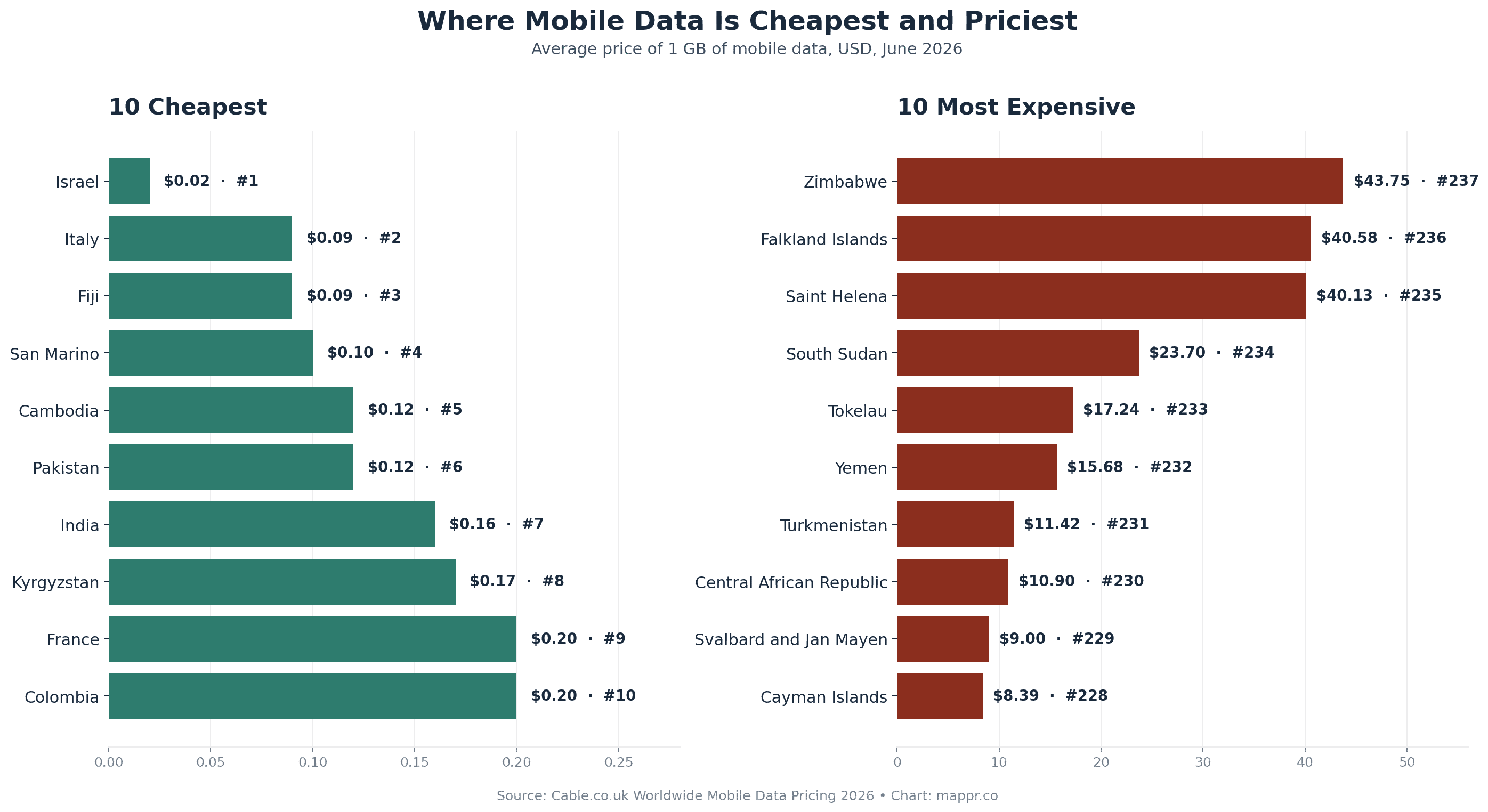

The 10 Cheapest and 10 Most Expensive

Israel is a full 4.5× cheaper than the next country in the ranking. Its runners-up are a curious pairing: Italy and Fiji tie at $0.09, followed by San Marino ($0.10) and then Cambodia and Pakistan ($0.12). At the other end, six countries pay over $10 per GB, and the top three all exceed $40, comfortably 1,000× the Israeli rate.

Why Israel Wins on Price

Israel’s $0.02 per GB is the product of a specific market design. In 2012 the country’s ministry of communications forced a wave of MVNO competition into a previously three-operator market. Cellcom, Partner and Pelephone found themselves competing against Golan Telecom, Hot Mobile and a growing list of second-tier resellers, and prices collapsed. Unlimited or very-high-allowance plans became the norm within about three years, and the average price per GB has been at or near the bottom of the Cable.co.uk ranking every year since 2019.

Similar dynamics explain the rest of the top ten. Italy has seen fierce price wars since Iliad’s 2018 entry; Fiji runs on a small number of very generous prepaid data buckets that average out low. Cambodia and Pakistan have young, mostly-mobile-only populations where operators compete on massive data bundles rather than voice minutes. India’s Reliance Jio launched with essentially free data in 2016 and reset the entire market’s price curve; Kyrgyzstan and other Central Asian markets have followed a similar template.

Why the US, Canada and Switzerland Cost So Much

The wealthy-but-expensive club is the story that keeps getting told and keeps not changing. Twelve of the world’s most developed democracies pay more per GB than roughly 90% of the countries below them. Half of them pay more than double the global average.

The pattern is not simply about wealth. Australia ($0.44), Denmark ($0.69) and Germany ($2.14) show that a rich country can still deliver competitive prices. The differentiating factor is market structure. The US and Canada both have concentrated three-operator markets (Verizon/AT&T/T-Mobile and Rogers/Bell/Telus) with limited MVNO competition and vast rural coverage obligations that get built into consumer pricing. Switzerland runs a similar three-operator setup (Swisscom/Sunrise/Salt) with high-touch premium service, and cross-border roaming reciprocity that keeps domestic prices from cratering. All three countries have historically underinvested in the kind of aggressive MVNO layer that broke prices in Israel, France and the UK.

The other pattern in the wealthy-but-expensive club is geographic: New Zealand ($5.89), Japan ($3.48) and South Korea ($5.01) are all small-population markets separated from the nearest big competitor by ocean. Norway ($4.07) is a similar case with sparse population and high per-tower costs. Roaming into a neighbouring cheap market is not a realistic pressure on domestic pricing when the neighbour is a two-hour flight away.

Where Mobile Data Is Truly Unaffordable

Zimbabwe’s $43.75 is the tail-end of a set of markets where the pricing tells a story about state, sanctions and infrastructure. The most expensive ten countries in the June 2026 ranking are:

- Zimbabwe ($43.75): hyperinflation, dollarised operator costs, tiny formal data plan market. Most Zimbabweans buy $1 daily bundles that translate to a very high per-GB rate.

- Falkland Islands ($40.58) and Saint Helena ($40.13): Sub-Atlantic islands with a single satellite-backhaul operator and no realistic competition.

- South Sudan ($23.70) and the Central African Republic ($10.90): Post-conflict states where operator networks are limited and financing costs are extreme.

- Tokelau ($17.24): A New Zealand territory of ~1,500 people; a satellite-only market by definition.

- Yemen ($15.68): Nearly a decade of war has fragmented the mobile network into de facto operator monopolies in Sanaa, Aden and Hodeidah.

- Turkmenistan ($11.42): A state-owned monopoly (TMCell) with no real domestic competition, plus heavy filtering.

- Svalbard and Jan Mayen ($9.00): Arctic operator serving fewer than 3,000 people.

- Cayman Islands ($8.39): High-income territory with two operators and generally premium pricing.

The unifying feature is not poverty. It is lack of competition. Extremely small populations, single-operator markets, satellite-only backhaul and post-conflict fragmentation all produce the same outcome: a per-GB rate 10–20× the global average.

The Seven-Year Trend: Prices Fall, the Gap Widens

The Cable.co.uk global average has fallen every year since the survey began:

- 2019: $8.18 per GB (global average)

- 2020: $5.25

- 2021: $4.07

- 2022: $3.12

- 2023: $2.59 (first year at the current level)

- 2024: $2.59

- 2025: $2.59

- 2026: $2.59

The 68% decline over seven years is real, but it has plateaued since 2023. The median country now pays about a third of what it did in 2019, largely thanks to 4G/5G rollouts and MVNO competition entering more markets. But the top and bottom of the ranking have diverged. In 2019, the priciest country charged about 3,700× the cheapest. In 2026 it is closer to 2,200×, narrower, but only because Zimbabwe fell out of a higher band, not because Israel got more expensive.

Methodology Notes

Cable.co.uk collects 5,603 mobile data plans across 237 countries and territories, converts local-currency prices to US dollars at the time of the survey, and calculates each country’s mean price per GB across all its plans. The June 2026 update reflects data gathered over roughly 3.5 weeks in mid-2026. Plans include prepaid, postpaid and data-only SIM offerings but exclude roaming, eSIM and travel packages. Rankings can shift when local operators launch new bundles or exchange rates move; the ordering is a snapshot, not a forecast.

One important caveat: the “average price per GB” here is a mean across each country’s surveyed plans, not the price the median consumer actually pays. In markets with a mix of very cheap unlimited plans and expensive premium tiers, the mean can be pulled up or down. It is the best cross-country comparison available, but consumer bills within any given country can vary widely.

What Comes Next

Three shifts are likely to keep reshaping the map. First, Starlink and other LEO satellite operators are pushing per-GB pricing down in exactly the markets where terrestrial data has been most expensive: remote islands, sparsely populated Nordic areas, and post-conflict states. The Cayman Islands and Svalbard rankings could compress meaningfully by 2027. Second, MVNO liberalisation in Canada (mandated wholesale access) and continued pressure on the US “big three” from Dish Network and cable-MVNOs like Xfinity Mobile could nudge North American prices closer to the global average. Third, 5G Standalone rollouts in Asia and Europe will keep pushing the cheap end further down, while the expensive end is likely to hold near current levels because the economics of small isolated markets do not change.

The underlying pattern will probably stay stable: mobile data is cheap where markets are competitive and dense, and expensive where they are not. Wealth, on this map, is a poor predictor.

Sources:

Primary data