Key Takeaways

- EU Inc is real, and moving fast. The European Commission published the formal proposal for the 28th Regime (EU Inc) on 18 March 2026. It creates an optional, EU-wide corporate form: one online incorporation, one common register, valid across all 27 Member States, with a stated target of adoption before end of 2026.

- Under €100 and 48 hours, on paper. The Commission's headline promise: incorporation capped at under €100, one online filing, decision within 48 hours, and no minimum share capital. A single digital company that can operate anywhere in the EU without re-registering.

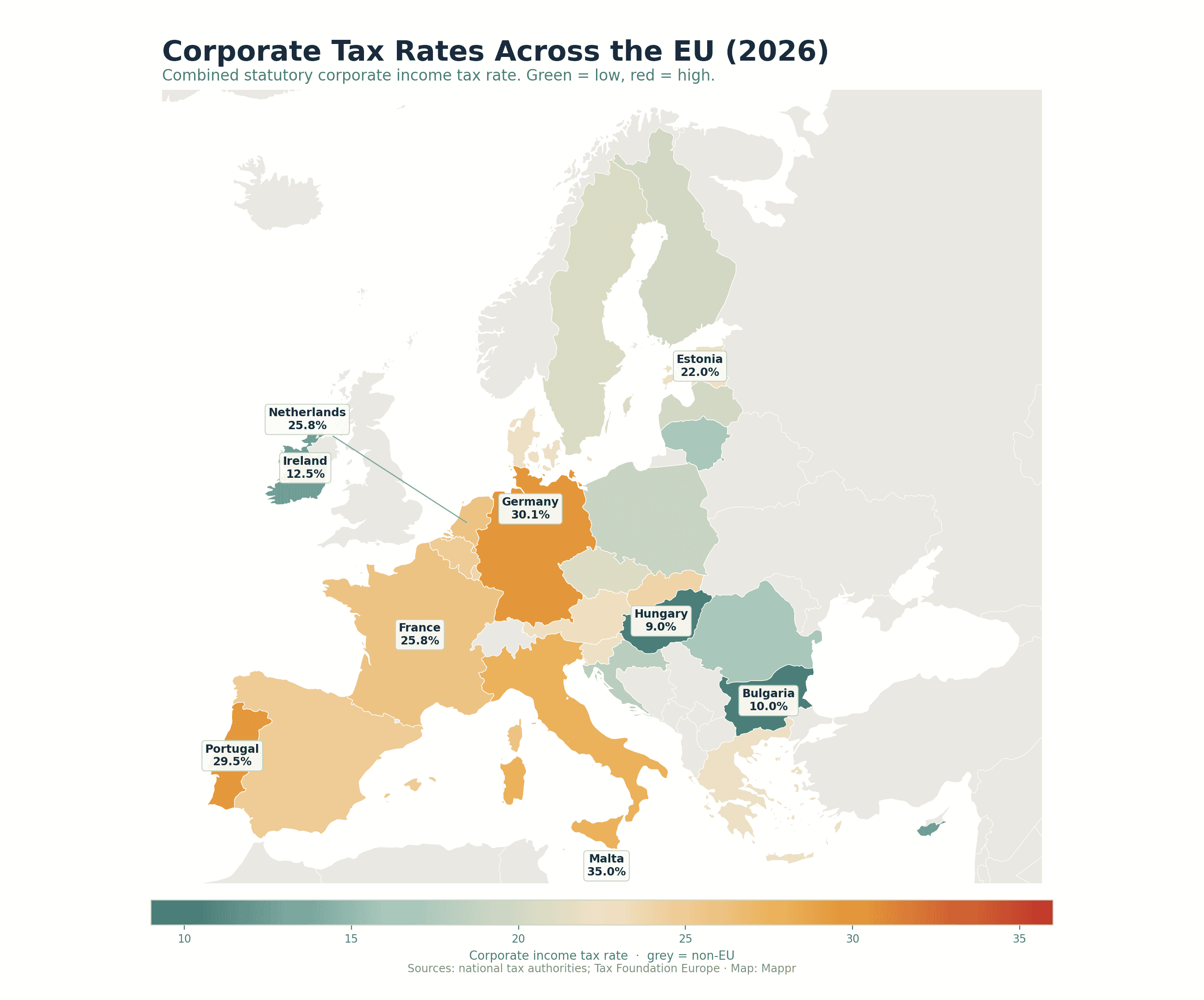

- Meanwhile, the national picture is a patchwork. Today, incorporating a limited company still costs anywhere from €50 in Ireland to well over €1,000 in Germany, the Netherlands or Luxembourg. Minimum share capital ranges from €0 in Finland to €25,000 in Germany. Corporate tax rates run from 9% in Hungary to 35% in Malta.

- Where you incorporate is only half the tax question. Founder personal tax residency, the company's place of effective management (POEM) and any permanent establishment can pull tax obligations toward jurisdictions the founder never intended. EU Inc will not change any of that.

- This is a map, not tax advice. Corporate law, tax rates and residency rules change; personal circumstances vary enormously. Anyone actually incorporating in the EU should consult a qualified lawyer and tax adviser in the target country.

Right now, if you want to run a company across the European single market, you still have to pick a country. You incorporate a French SAS, a German GmbH or an Estonian OÜ, and then, when you expand, you re-do most of it in every other country you enter. It is the biggest paper wall inside the world’s second-largest market, and 27 different sets of company law sit behind it.

The 28th Regime, better known by the campaign name EU Inc, is the European Commission’s attempt to punch through that wall. The formal proposal was published on 18 March 2026, and the political target is adoption before the end of the year. Here is what it would actually cost, how it compares to the 27 national alternatives available today, and, crucially, what it would not change about tax.

What EU Inc Would Actually Deliver

EU Inc creates an optional 28th corporate form, sitting alongside the existing 27 national ones. Any founder in any Member State could choose to incorporate under it instead of, say, a Dutch BV. The Commission’s stated design goals are:

- One online incorporation, done in a single filing.

- A stated target of 48 hours to receive the decision.

- Registration cost capped at under €100, everywhere.

- No minimum share capital.

- A common EU business register with a "once-only" data principle so the same information is not re-collected by every Member State.

- A European business wallet holding company credentials that any EU public administration must accept.

For a startup founder in Berlin who wants to hire in Portugal and Poland without setting up two subsidiaries, this is a genuinely large change. For a two-person software company that just wants to be legally incorporated somewhere sensible, it may be the simplest option ever offered inside the EU.

The Roadmap: How EU Inc Actually Becomes Law

| Date | Milestone |

|---|---|

| Sep 2024 | Draghi Report on European competitiveness calls for a unified EU corporate form. |

| Apr 2024 | Letta Report echoes the recommendation in the context of the Single Market. |

| May 2025 | EU Startup and Scale-up Strategy sets out the “28th Regime” concept, backed by a coalition of 15+ European VCs and founders under the "EU Inc" label. |

| Sep 2025 | Public consultation closes with 870+ stakeholder responses. |

| Jan 2026 | European Parliament adopts own-initiative recommendations. |

| Mar 2026 | European Commission publishes the formal Regulation proposal for EU Inc. Endorsed by the European Council 19-20 March. |

| Apr – May 2026 | Council Working Party negotiations begin (17 Apr, 27 Apr, 7 May). |

| Target: end-2026 | Adoption by Council and Parliament (political target set by the Council). |

| 2027 (est.) | Earliest incorporation of the first EU Inc companies. |

This is a Regulation, not a Directive. Once adopted, it applies directly in every Member State without national transposition. That is why the Commission and Council are pushing hard for the end-of-2026 target: unlike the Directive on Cross-Border Conversions, national legislatures do not each get a second go.

Meanwhile, Here Is the National Picture

Every EU-27 country still has a limited-company form of its own, and none of them look much like each other. The pattern for basic incorporation, before you get anywhere near tax, splits into four camps:

- The near-free digital picks: Estonia, Ireland, Finland, Portugal, France and Spain all let you incorporate with essentially €1 of share capital and a few hundred euros of formalities. Estonia’s e-Residency machine registers a company in about a day and costs around €265 all in.

- The still-affordable but paperwork-heavy: Germany’s GmbH, the Netherlands’ BV in practice, Luxembourg’s Sàrl and Italy’s SRL all involve a notary. Costs run €1,000 to €3,000 and, in Germany’s case, €25,000 of authorized capital (though only half needs to be paid in).

- The Central and Eastern European bargain: Bulgaria, Romania, Hungary and Czechia all have very low nominal minimum capital and low registration fees, though local language and residency requirements can complicate the picture in practice.

- The Nordic middle: Sweden and Denmark still require a few thousand euros of paid-in capital, but the registration itself is fast and cheap.

The Full 27-Country Comparison

Common SME entity, minimum share capital, typical formation cost, corporate income tax rate and the withholding rate a non-resident individual shareholder would face on dividends. Sortable and searchable. Estimates: exact figures depend on advisors used, notary fees and share structure.

| Country | Common SME entity | Minimum share capital | Typical formation cost | Corporate tax rate | Dividend withholding (non-resident) |

|---|---|---|---|---|---|

| Austria | GmbH | 10,000 | €700 – 1,500 | 23.0% | 28% |

| Belgium | SRL/BV | €1 | €900 – 1,500 | 25.0% | 30% |

| Bulgaria | OOD | €1 | €200 – 400 | 10.0% | 5% |

| Croatia | d.o.o. | €2,500 | €500 – 900 | 18.0% | 10% |

| Cyprus | Ltd | €1 | €1,000 – 2,000 | 12.5% | 0% |

| Czechia | s.r.o. | €0.05 | €400 – 800 | 21.0% | 15% |

| Denmark | ApS | €2,700 | €500 – 1,000 | 22.0% | 27% |

| Estonia | OÜ | €0.01 | €265 (online) | 22.0% | 0% |

| Finland | Oy | €0 | €275 – 400 | 20.0% | 20% |

| France | SARL / SAS | €1 | €200 – 800 | 25.8% | 25% |

| Germany | GmbH | €25,000 | €500 – 1,500 | 30.1% | 26% |

| Greece | IKE | €1 | €60 – 300 | 22.0% | 5% |

| Hungary | Kft | €7,700 | €200 – 400 | 9.0% | 15% |

| Ireland | Ltd | €1 | €50 – 300 | 12.5% | 25% |

| Italy | SRLS / SRL | €1 (SRLS) / €10,000 | €1,500 – 3,000 | 27.8% | 26% |

| Latvia | SIA | €2,800 | €300 – 600 | 20.0% | 0% |

| Lithuania | UAB | €1,000 | €300 – 600 | 17.0% | 15% |

| Luxembourg | Sàrl | €12,000 | €1,500 – 3,000 | 23.9% | 15% |

| Malta | Ltd | €1,165 | €250 – 500 | 35.0% | 0% |

| Netherlands | BV | €0.01 | €1,000 – 2,000 | 25.8% | 15% |

| Poland | sp. z o.o. | €1,160 | €300 – 700 | 19.0% | 19% |

| Portugal | Lda | €1 | €360 (SME desk) | 29.5% | 28% |

| Romania | SRL | €0.20 | €100 – 300 | 16.0% | 8% |

| Slovakia | s.r.o. | €5,000 | €330 – 600 | 24.0% | 7% |

| Slovenia | d.o.o. | €7,500 | €200 – 400 | 22.0% | 25% |

| Spain | SL | €1 | €150 – 500 | 25.0% | 19% |

| Sweden | AB | €2,200 | €200 – 400 | 20.6% | 30% |

Two important caveats built into that table. First: Estonia is unique. Its 22% headline rate only applies to distributed profits. Retained and reinvested profits are taxed at 0%, which is why it is the go-to for scaling founders who plan to plow earnings back in. Second: Malta’s 35% is a headline. Its refund system means the effective rate for non-resident shareholders is typically around 5-6%, which is why it appears expensive and is not.

The Tax Triangle: Where Founders Get Caught

The most important thing to understand about EU corporate tax is that incorporation is only one leg of a triangle. Two others matter just as much, and EU Inc will not change any of them.

1. The founder’s personal tax residency

This determines where your salary, dividends and capital gains are taxed. It is generally driven by where you spend more than 183 days a year (with several other tests). Being tax-resident in France while owning a German GmbH means France taxes your German dividends at French personal rates, subject to a treaty credit for the withholding tax. If you move without careful planning, exit tax rules in France, Germany, the Netherlands, Denmark and now Spain can trigger a deemed sale of your shares.

2. The company’s place of effective management (POEM)

This determines where the company itself is tax-resident, and it can override the country of incorporation. Under the OECD tie-breaker rule embedded in essentially every EU tax treaty, if a company is incorporated in Cyprus but its board meets, its CEO works, and its strategic decisions are made in Amsterdam, the Netherlands can claim it as a Dutch tax resident, at Dutch rates, on worldwide profits. This is not theoretical: post-Brexit and post-2020, tax authorities have become far more aggressive about POEM.

3. Permanent establishment (PE)

This is the country-in-the-middle case. Even if your company is fully resident somewhere else, hiring a full-time salesperson working from her home in Milan can create an Italian permanent establishment, and Italy can tax the profits attributable to that activity at Italian rates. Since the pandemic, home-office PE has become the single most litigated cross-border tax issue in Europe.

None of that changes when EU Inc arrives. An EU Inc company will still have a POEM somewhere. Its employees will still create PE risk wherever they physically work. The Regulation streamlines registration, not the underlying tax architecture.

EU Inc vs Incorporating Locally

Assuming EU Inc launches on schedule in 2027, the choice for a European founder will look roughly like this:

| EU Inc (from 2027) | National limited company (today) | |

|---|---|---|

| Incorporation cost | Under €100 (capped) | €50 to €3,000 depending on country |

| Speed | Target 48 hours, one filing | 1 day (Estonia) to several weeks (Germany, Italy) |

| Minimum capital | None | €0 in Finland to €25,000 in Germany |

| Recognised where? | Automatically in all 27 EU countries | In the country of incorporation; separate branches or subsidiaries elsewhere |

| Corporate tax rate | Determined by where the company is tax-resident (POEM), not by EU Inc itself | Determined by country of incorporation, and by POEM if it differs |

| Best for | Startups planning multi-country hiring and expansion from day one | Single-country businesses; anyone wanting a specific tax regime (Estonian deferral, Irish 12.5%, Cypriot 0% dividend WHT) |

| Watch out for | Still being negotiated; may include carve-outs (financial services, some regulated sectors) | Notary and language requirements; capital lock-ups; slow registration in the biggest markets |

The short version: EU Inc solves the "incorporate once, operate anywhere" problem. It does not solve the "where do I pay tax" problem, and it is not designed to. A well-advised founder in 2027 will still be picking a tax residency for herself, choosing a management setup for the company, and then deciding whether the streamlined 28th Regime beats her best national alternative on formation. For a large minority of European founders, it probably will.

This is a map, not tax advice. Any actual incorporation deserves a qualified lawyer and tax adviser in the target country. But for the first time in EU history, “somewhere in the EU” is on its way to being a real, single answer.

Sources: