Key Takeaways

- Eurozone composite hits 52.2 — a 47-month high. S&P Global / HCOB Eurozone Manufacturing PMI rose to 52.2 in April 2026 from 51.6 in March, the highest reading since May 2022. PMI above 50 = factory-sector expansion.

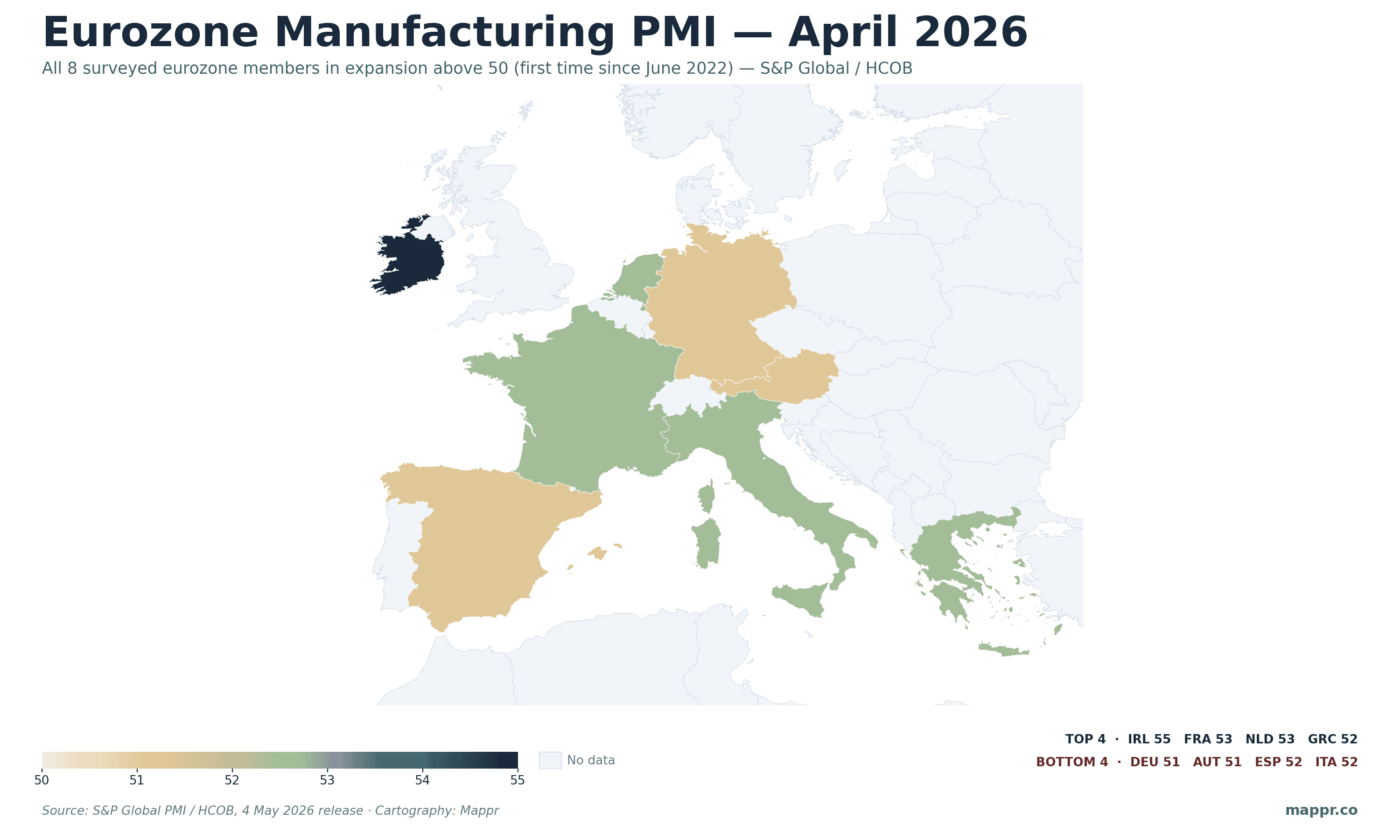

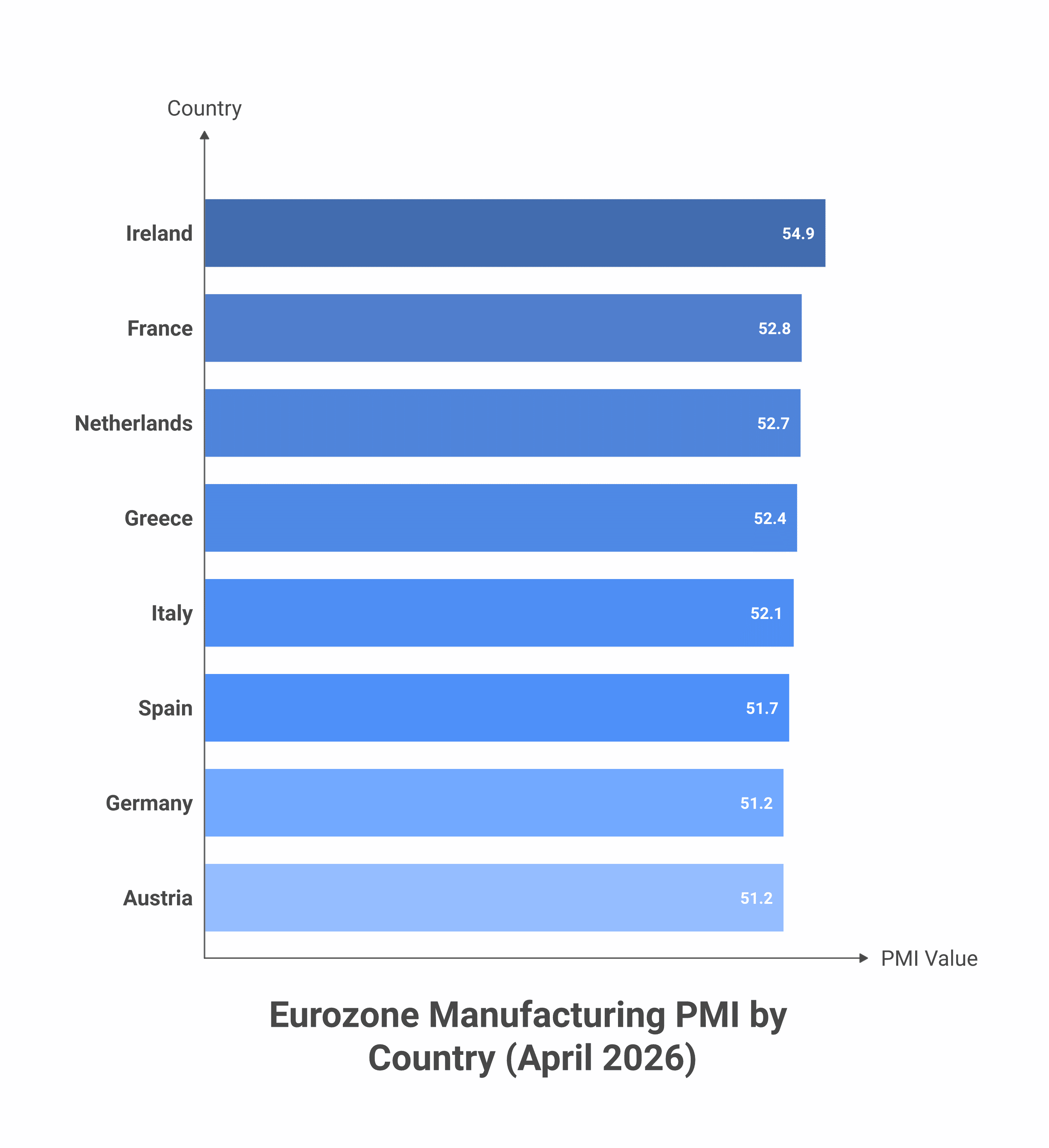

- Ireland leads at 54.9. Ireland's AIB Manufacturing PMI rose to 54.9 in April from 53.7 in March — the strongest reading since May 2022, and the highest of the 8 surveyed eurozone members.

- France and Italy posted their sharpest expansions since H1 2022. France's HCOB PMI jumped to 52.8 (above the 49.5 expected) and Italy's rose to 52.1 from 51.3. Spain was the biggest mover — up to 51.7 in April from 48.7 in March, a 3-point swing.

- Headline strength masks tariff anxiety. S&P Global's chief economist Chris Williamson called the rise "more a cause for alarm than celebration" — production and order books are being inflated by stockpiling ahead of expected price hikes and supply disruptions, with input price inflation at a 46-month high and business optimism at its lowest since November 2024.

The eurozone’s manufacturing sector posted its strongest improvement in nearly four years in April 2026. The S&P Global Eurozone Manufacturing PMI — a composite of new orders, output, employment, suppliers’ delivery times, and stocks of purchases across the bloc — rose to 52.2 in April from 51.6 in March. That’s the highest reading since May 2022, and the first time since June 2022 that all eight of the surveyed eurozone members posted readings above the 50 no-change line.

The news angle is the breadth of the expansion: Ireland leading at 54.9 (its highest in 47 months), France and Italy posting their sharpest expansions since the first half of 2022, Spain swinging from contraction (48.7 in March) into solid growth (51.7 in April), and Germany and Austria still expanding even as their pace slipped slightly. The data was collected April 9–23, just as the front-loading effect of expected US tariff increases began driving European customers to bulk-order ahead of price changes.

This post maps the country-by-country picture and unpacks why S&P Global’s chief economist Chris Williamson called the rise “more a cause for alarm than celebration” — a counter-intuitive read on what looks like a textbook recovery print.

📋 April 2026 Eurozone Manufacturing PMI — Country-by-Country

Final readings for all 8 surveyed eurozone members, ranked by April 2026 PMI score. Movement column shows the change from March 2026.

| Rank | Country | Apr 2026 PMI | Mar 2026 PMI | Movement | Notes |

|---|---|---|---|---|---|

| 1 | 🇮🇪 Ireland | 54.9 | 53.7 | ▲ +1.2 | Highest since May 2022 (47-month high). AIB-sponsored survey. |

| 2 | 🇫🇷 France | 52.8 | 49.9 | ▲ +2.9 | Sharpest expansion since H1 2022. Beat 49.5 consensus by a wide margin. |

| 3 | 🇳🇱 Netherlands | 52.7 | 52.7 | ■ 0.0 | Same reading as March. Steady solid expansion. |

| 4 | 🇬🇷 Greece | 52.4 | 54.5 | ▼ -2.1 | Down from a strong March print but still well in expansion territory. |

| 5 | 🇮🇹 Italy | 52.1 | 51.3 | ▲ +0.8 | Sharpest expansion since H1 2022 alongside France. |

| 6 | 🇪🇸 Spain | 51.7 | 48.7 | ▲ +3.0 | Biggest mover — flipped from contraction to solid expansion. |

| 7 | 🇩🇪 Germany | 51.2 | 52.2 | ▼ -1.0 | Slight slowdown but still in expansion. Largest manufacturing economy in the bloc. |

| 8 | 🇦🇹 Austria | 51.2 | 52.4 | ▼ -1.2 | UniCredit Bank Austria PMI; loss of momentum but holds expansion. |

| — | 🇪🇺 Eurozone composite | 52.2 | 51.6 | ▲ +0.6 | 47-month high. All 8 above 50 — first time since June 2022. |

What Is the Manufacturing PMI?

The Purchasing Managers’ Index (PMI) is one of the most-watched leading indicators in macroeconomics. It’s compiled monthly by S&P Global Market Intelligence (rebranded from IHS Markit in 2022) from survey responses sent to purchasing managers at around 3,000 private-sector manufacturers across the eurozone. Each respondent answers whether key business variables — new orders, output, employment, suppliers’ delivery times, and stocks of purchases — are higher, the same, or lower than the previous month.

The diffusion-index methodology produces a single number between 0 and 100. Above 50 = expansion; below 50 = contraction; 50 = no change. The headline Manufacturing PMI is a weighted average: New Orders 30%, Output 25%, Employment 20%, Suppliers’ Delivery Times 15%, Stocks of Purchases 10%. The Eurozone composite weights national readings by each country’s share of eurozone manufacturing value added (Eurostat figures).

PMI prints typically arrive about a month before official industrial production statistics, which is why central banks and financial markets give them outsized weight. A move above 50 after a contraction signals factory output is growing; a move from 51 to 52 signals it’s growing FASTER than the previous month. Historical eurozone Manufacturing PMI ranges: low of 33.4 in April 2020 (COVID lockdowns), high of 63.4 in May 2021 (post-COVID rebound), and a long stretch below 50 through 2023–early 2025 during the bloc’s industrial slump.

The Country Stories Behind April’s Reading

🇮🇪 Ireland (54.9) — The Standout

Ireland’s AIB Manufacturing PMI hit 54.9 in April, its highest reading since May 2022. The Irish print typically diverges from continental Europe because Irish manufacturing is dominated by pharmaceuticals, medical devices, and tech-sector intermediate goods — categories that face very different demand cycles than German automotive or French chemicals. April’s strength reflects continued post-pandemic restocking by US-bound pharma exports plus front-loading ahead of expected US tariff changes.

🇫🇷🇮🇹 France & Italy — Sharpest Expansions Since 2022

The most-watched country-level prints in this batch were France (52.8 vs. 49.5 expected) and Italy (52.1 vs. 51.9 expected). Both posted their fastest manufacturing expansions since the first half of 2022 — pre-energy-shock, pre-rate-hike, pre-Ukraine-war-disruption. The narrative is twofold: a genuine improvement in consumer-facing manufacturing (cars, appliances) plus a substantial front-loading of orders by customers worried about supply disruptions in coming months.

🇪🇸 Spain — The Biggest Mover (+3.0pp)

Spain’s HCOB PMI swung from 48.7 in March (contraction) to 51.7 in April (solid expansion) — a 3.0-point jump that beat the 49.5 consensus by 2.2 points. The Spanish industrial cycle has been one of the more volatile in the bloc, oscillating around 50 since mid-2024. April’s reading suggests the long-running weakness in capital-goods demand may be turning, with new orders rising for the first time in five months.

🇩🇪 Germany & 🇦🇹 Austria — Slight Slowdown, Still Expanding

Germany — by far the largest manufacturing economy in the bloc — printed 51.2, down from 52.2 in March. The Ifo Business Climate Index (a separate but correlated indicator) also softened to 84.4. The German softening is partly a base effect (March’s reading was unusually strong) and partly reflects continued weakness in automotive demand from China. Austria’s UniCredit-sponsored PMI also slipped, from 52.4 to 51.2, with both new orders and output declining at the margin even though the headline stays in expansion.

🇳🇱 Netherlands & 🇬🇷 Greece — Steady at the Top

The Netherlands held at 52.7 (the same as March) — solid, predictable, second-best in the bloc. Greece printed 52.4, down from a strong 54.5 in March but still firmly in expansion. Both economies have been net beneficiaries of supply-chain reshuffling in the post-pandemic period: the Netherlands as a logistics-and-machinery hub, Greece as a low-cost manufacturing alternative within the EU customs perimeter.

⚠️ Why S&P Global Is Cautious About This Print

The most striking quote from the press release came from Chris Williamson, S&P Global Market Intelligence’s chief business economist: “Although the PMI has risen to its highest for nearly four years, the survey is more a cause for alarm than celebration. Production and order books are being buoyed by the building of safety stocks as a result of widespread concerns over supply.”

That’s an unusual framing for a strong reading. Three sub-indices behind the headline support the cautious interpretation:

- Input price inflation hit a 46-month high. Since February the seasonally-adjusted Input Prices Index has jumped 19 points. Output charge inflation accelerated to its sharpest pace since January 2023.

- Suppliers’ delivery times worsened. Stocks of purchases were depleted but at a less pronounced rate than March, with respondents citing front-loaded demand and tariff-related supply concerns as the main drag on lead times. Delays were the worst since July 2022.

- Business optimism dropped to a 6-month low. The forward-looking Future Output Index slumped to its lowest since November 2024, even as the current-month headline rose. Manufacturers are reading the strong April orders as a one-off pull-forward, not a durable trend.

Translation: the headline says factories are running hot, but the survey’s leading components say it’s the calm-before-the-storm flavor of running hot. If front-loading is responsible for the spring surge, expect a reversal once tariff pricing settles and inventories normalise — likely in Q3 2026.

What to Watch Next

- May Manufacturing PMI flash readings (May 22): if the May print holds above 52, the front-loading thesis weakens. If it pulls back to 50–51, that supports the “calm before the storm” interpretation.

- ECB June meeting: the Governing Council will weigh sustained PMI strength against the cooling sub-indices. A strong May print could delay the next rate cut beyond the markets’ current pricing.

- Country dispersion: the gap between Ireland’s 54.9 and Germany’s 51.2 is unusually wide. Watch whether convergence happens via German recovery or Irish moderation in coming months.

- Stock cycle reversal: the eurozone manufacturing inventory drawdown of late 2024–early 2025 may be ending. If true, output growth in the next 1-2 quarters depends on whether end-demand confirms the new orders trend.