Key Takeaways

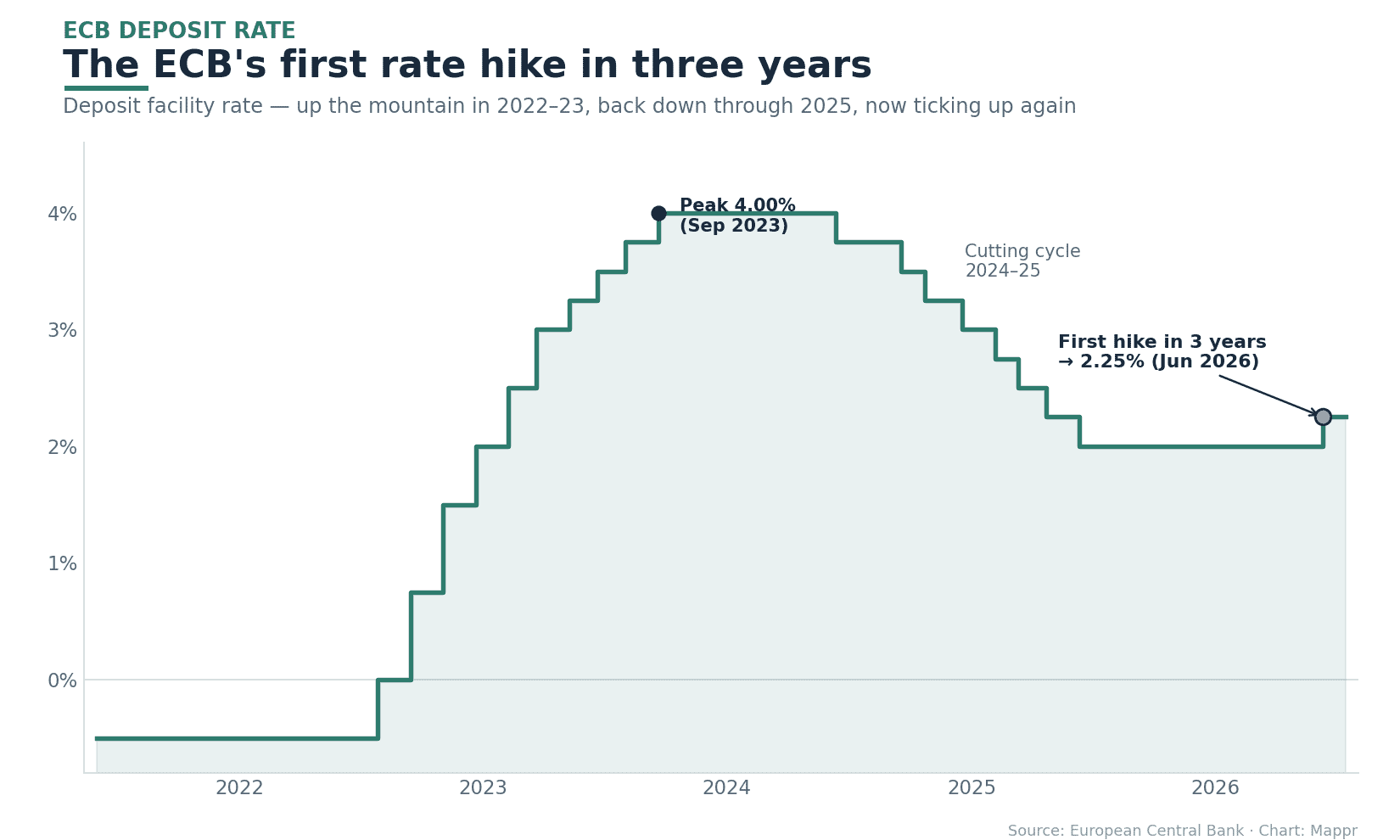

- The first hike since 2023. The ECB raised its deposit rate by 0.25 points to 2.25% on June 11, 2026 — its first increase in three years

- An energy shock is the trigger. Eurozone inflation has climbed back to about 3.2%, pushed up by the oil-price spike from the Strait of Hormuz crisis

- Up the mountain and most of the way back down. Rates peaked at 4.0% in 2023, were cut all the way to 2.0% by mid-2025, and are now ticking up again

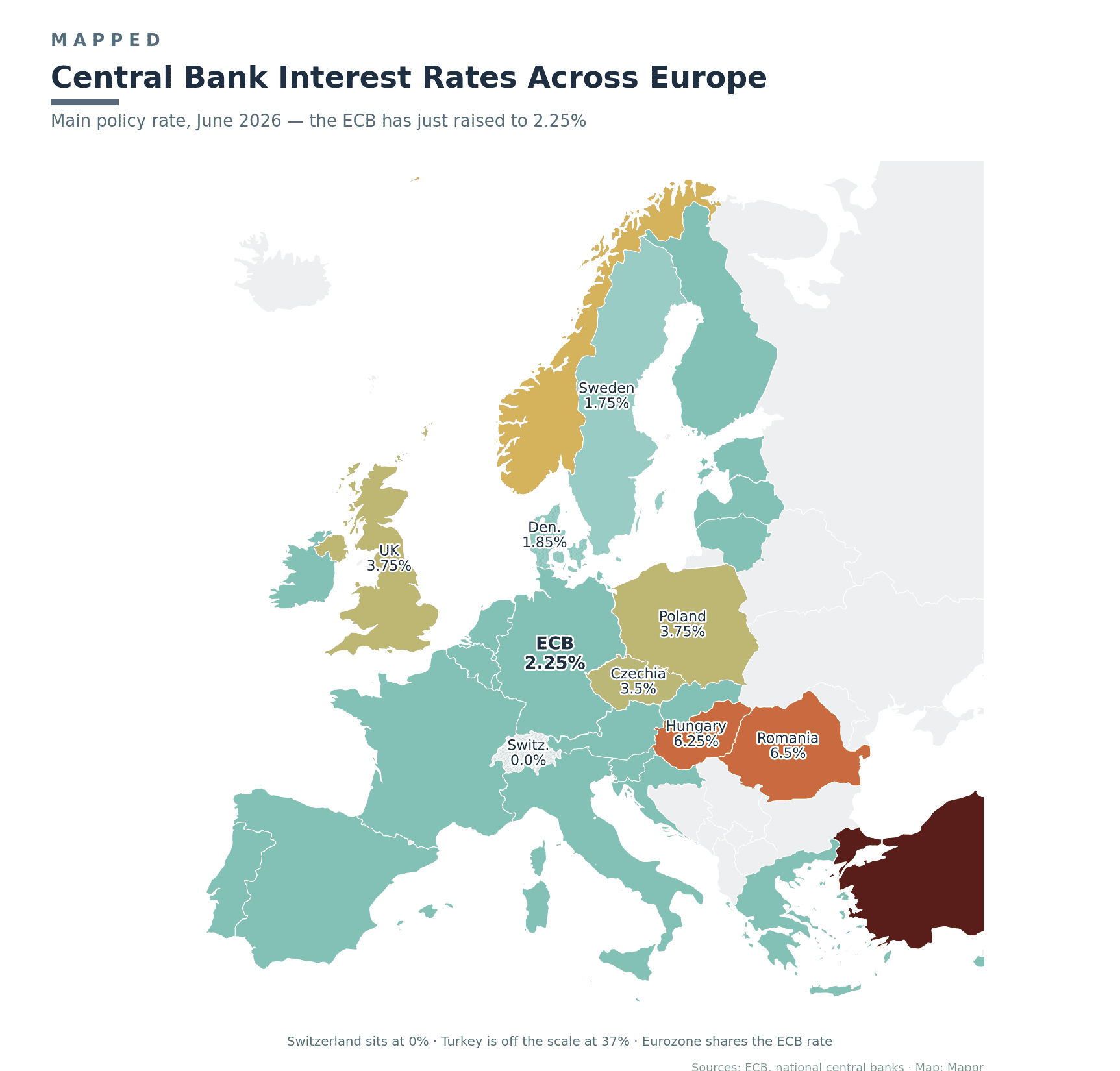

- Europe's rates vary enormously. Switzerland sits at 0% and the eurozone at 2.25%, while Turkey is in a different world at 37%

- Borrowers feel it first. Households on tracker mortgages across the eurozone face higher repayments straight away

The European Central Bank has raised interest rates for the first time in three years, lifting its key deposit rate by a quarter point to 2.25% on June 11, 2026. It is a notable turn: after an aggressive hiking cycle in 2022–23 and a steady run of cuts through 2024–25, the ECB is tightening again — and the reason traces back to the oil fields of the Gulf.

What the ECB Did

At its June 11 meeting, the ECB lifted the deposit facility rate from 2.00% to 2.25%, and the main refinancing rate to 2.40%. It is the first increase since September 2023 — the month rates peaked at 4.0% at the top of the post-pandemic inflation fight. After holding at 2.0% since mid-2025, policymakers judged that price pressures had returned strongly enough to act.

Why Now: The Energy Shock

The trigger is inflation, and the inflation is mostly about energy. Eurozone consumer prices rose to around 3.2% in the spring of 2026, up from roughly 1.9% in February and well above the ECB’s 2% target. The surge has been driven by the spike in oil prices flowing from the Strait of Hormuz crisis — roughly a fifth of the world’s oil passes through that chokepoint, and the disruption fed straight into European fuel and power costs. With the conflict showing no sign of resolving, the ECB decided it could no longer wait it out.

How Europe’s Rates Compare

At 2.25%, the eurozone sits in the lower-middle of the European pack. Switzerland remains the outlier on the low side at 0.0%, while the Nordics are split — Norway is up at 4.25% and even hiking, while Sweden (1.75%) and euro-pegged Denmark (1.85%) sit below the ECB. Central and Eastern Europe runs hotter: Hungary at 6.25% and Romania at 6.5% top the EU, with Poland (3.75%) and Czechia (3.5%) in between. The UK is at 3.75%. And then there is Turkey, in a category of its own at 37% as its central bank battles a far deeper inflation problem.

From the Mountain to the Climb Back

The longer arc is striking. The ECB held its deposit rate below zero — at −0.5% — right up to mid-2022. Then came the fastest tightening in the euro’s history: ten hikes in just over a year took the rate to 4.0% by September 2023. As inflation cooled, the cuts began in June 2024 and ran steadily down to 2.0% by mid-2025. This week’s quarter-point move is small, but it reverses that direction for the first time — a signal that the era of falling rates may be on pause.

What It Means

For households, the most immediate effect lands on variable and tracker mortgages, which reprice almost at once; savers, conversely, get a little more on deposits. For the wider economy, a higher cost of borrowing is the ECB’s lever to cool demand — though when the inflation is coming from an oil shock rather than an overheating economy, the tool is blunter than usual. The bigger question is whether June’s hike is a one-off insurance move or the start of a new tightening cycle, and that will hinge largely on what happens next in the Gulf.

Interest-rate data and the June 2026 ECB decision.

Image Sources

- Mappr – Rate chart, Europe map and featured illustration created by Mappr